International Institute of Business & Tax Excellence Newsletter (IIBTE.com)

International Institute of Business & Tax Excellence Newsletter (IIBTE.com)

Edition 2 - March 2020

Welcome to the second edition of the IIBTE newsletter, welcome to edition 2!

The International Institute of Business & Tax Excellence is poised to harness globalization, one business at a time.

Edition 2 of the International Institute of Business & Tax Excellence Newsletter (IIBTE.com) is proudly sponsored by:

Coral International Asset Managers is an asset management company with over 30 years of experience. Coral has a dedicated team specializing in property management and manages an extensive portfolio across South Africa and internationally. Coral services a large existing client base and targets prospective clients in the residential, commercial and retail property markets.

At Coral, we strive for service excellence by providing our clients with the best property management services. Coral approaches each of their property ventures with the aim of increasing long term value whilst ensuring maximum operating efficiency and client satisfaction.

In this edition:

Benefits of Flexible Work Schedules

by Nazneen Adam of Coral International Asset Managers (Pty) Ltd

www.coralassetmanagers.comAccounting Methodologies – The Elements of Financial Statements: Assets

by Azhar Mia of Kreston KZN

www.krestonsa.com/kznWhat is the Coronavirus disease 2019 (COVID-19) & how has it impacted the world economy thus far?

by Mohammed Essack of Coral International Asset Managers (Pty) Ltd

www.coralassetmanagers.comArticle 1:

Benefits of Flexible Work Schedules

A study commissioned by Citrix found that 93% of South African IT decision makers agree that technology contributes to increased employee productivity but 80% of those respondents still believe that employees are more productive when in an office environment as opposed to working remotely. This research surveyed 250 IT decision makers in South Africa and it revealed that 58% of employers perceived themselves to be more productive when working remotely whilst a low 7% said that they were less productive when working flexibly. It is fascinating to note that there is disparity to this extent between the potential productivity of employers and employees. (Business Tech, 2019)

Flexible work arrangements have a number of benefits for both the employer and employee. Some of these benefits as mentioned of which I have expanded on, listed on the SHRM (2020) website include:

Improve workers’ drive and/or morale. Workers may feel increased motivation and drive to complete the necessary tasks for their employers.

Reducing absenteeism. Flexible work schedules will allow employees to work around the responsibilities that may cause them to require time off from their jobs. If they are able to manage their own time and plan their tasks – it can assist in reducing absenteeism.

Improving the retention of good workers. Talent is a valuable commodity in the recruiting world and being able to retain a worker that is good and has knowledge of the business is paramount.

Improve employee productivity. A boost in productivity can be achieved by employees feeling calmer and less stressed at work as their other non-work obligations are being fulfilled. They may offer more focus to their tasks at work and improve performance.

Create a balance between an employee’s work life and their personal life. Some people have other interests that they are passionate about and some have family obligations that they have to successfully balance with work responsibilities. By having an option to redirect time to other, important tasks – the employee has a chance to achieve their goal of balance.

Positioning the employer as an attractive one when recruiting. The goal is to gain the best talent from the pool of candidates that exist, and with the need for more flexible work schedules – employers can have an advantage over other businesses competing for the same.

Having a positive effect on the environment by reducing the workplaces ‘footprint’. With less vehicles on the road and less buildings being used for office spaces – it can contribute to a positive environmental impact.

Paul Burrin, the VP at Sage People discusses flexible working schedules on the IOL website and cites that their research have shown that 66% of workers surveyed want to feel valued and trusted. The freedom that employees are given when they are able to plan their own time to achieve their work goals, allows them to feel recognised and most importantly, trusted.

In my opinion, as a working mother and wife – a flexible work schedule will allow me to spend time with a busy one-year old who needs my attention but also complete work-related tasks in the quiet hours. Whilst some tasks are almost impossible to perform remotely, there are admin related duties that can be completed with no need for a physical presence. With advances in technology raging forward at lightning speed, it would be counter-productive to consider the future of working and the idea of an office environment to be the only option to create productive employees.

Bibliography

Unknown Author (2020) Managing Flexible Work Arrangements.

https://www.shrm.org/resourcesandtools/tools-and-samples/toolkits/pages/managingflexibleworkarrangements.aspx (Accessed 06/03/2020)Staff Writer (2019) South African bosses have their say on flexible working.

https://businesstech.co.za/news/cloud-hosting/342945/south-african-bosses-have-their-say-on-flexible-working/ (Accessed 06/03/2020)Burrin, Paul (2019) 7 Reasons why you should promote flexible working hours.

https://www.iol.co.za/personal-finance/guides/7-reasons-why-you-should-promote-flexible-working-hours-18711306 (Accessed 06/03/2020)Unknown Author (2018) Why Flexible Work Schedules are Beneficial for Both Employees and Employers.

https://www.humanity.com/blog/why-flexible-work-schedules-are-beneficial-for-both-employees-and-employers.html (Accessed 06/03/2020)SABPP (2018) Flexible Work Practices

https://sabpp.co.za/wp-content/uploads/2018/04/Fact-Sheet_May-2018_v003-with-active-links.pdf (Accessed 06/03/2020)

Article 2:

Accounting Methodologies – The Elements of Financial Statements: Assets

INTRODUCTION

In March 2018, the International Accounting Standards Board (IASB) issued the revised Conceptual Framework for Financial Reporting (Conceptual Framework), a comprehensive set of concepts for financial reporting. At a minimum, the revised Conceptual Framework sets out the following:

the objective of financial reporting;

the qualitative characteristics of useful financial information;

definitions of an asset, a liability, equity, income and expenses.

The above mentioned revision entails updated definitions of an asset and liability.

The Conceptual Framework defines an asset as a present economic resource controlled by the entity as a result of past events (Conceptual Framework – Par. 4.4).

This article details 3 aspects of the definition.

RIGHT

Many rights are established by contract, legislation or similar means. For example, an entity might obtain rights from owning or leasing a physical object, from owning a debt or equity instrument, or from owning a registered patent (Conceptual Framework – Par. 4.7).

Rights that have potential to produce economic benefits take many forms, including:

rights to receive cash.

rights to receive goods and services.

rights to exchange economic resources with another party on favourable terms.

rights to benefit from an obligation of another party to transfer an economic resource if a specified uncertain future event occurs (Conceptual Framework – Par. 4.6).

In principle, each of an entity’s rights is a separate asset. However, for accounting purposes, related rights are often treated as a single unit of account that is a single asset. For example, legal ownership of a physical object may give rise to several rights, including:

the right to use the object;

the right to sell rights over the object;

the right to pledge rights over the object (Conceptual Framework – Par. 4.11).

POTENTIAL TO PRODUCE ECONOMIC BENEFITS

An economic resource is a right that has the potential to produce economic benefits. For that potential to exist, it does not need to be certain, or even likely, that the right will produce economic benefits. It is only necessary that the right already exists and that, in at least one circumstance, it would produce for the entity economic benefits beyond those available to all other parties (Conceptual Framework – Par. 4.14).

An economic resource could produce economic benefits for an entity by entitling or enabling it to do, for example, one or more of the following:

receive contractual cash flows or another economic resource;

exchange economic resources with another party on favourable terms;

produce cash inflows or avoid cash outflows by, for example: leasing the economic resource to another party.

receive cash or other economic resources by selling the economic resources; or

extinguish liabilities by transferring the economic resource (Conceptual Framework – Par. 4.16).

There is a close association between incurring expenditure and acquiring assets, but the two do not necessarily coincide. Hence, when an entity incurs expenditure, this may provide evidence that the entity has sought future economic benefits, but does not provide conclusive proof that the entity has obtained an asset. Similarly, the absence of related expenditure does not preclude an item from meeting the definition of an asset (Conceptual Framework – Par. 4.17)

CONTROL

Control links an economic resource to an entity. Assessing whether control exists helps to identify the economic resource for which the entity accounts. For example, an entity may control a proportionate share in a property without controlling the rights arising from ownership of the entire property. In such cases, the entity’s asset is the share in the property, which it controls, not the rights arising from ownership of the entire property, which it does not control (Conceptual Framework – Par. 4.19).

An entity controls an economic resource if it has the present ability to direct the use of the economic resource and obtain the economic benefits that may flow from it. Control includes the present ability to prevent other parties from directing the use of the economic resource and from obtaining the economic benefits that may flow from it. It follows that, if one party controls an economic resource, no other party controls that resource (Conceptual Framework – Par. 4.20).

Sometimes one party (a principal) engages another party (an agent) to act on behalf of, and for the benefit of, the principal. For example, a principal may engage an agent to arrange sales of goods controlled by the principal. If an agent has custody of an economic resource controlled by the principal, that economic resource is not an asset of the agent (Conceptual Framework – Par. 4.25).

BIBLIOGRAPHY

IFRS Standards – Conceptual Framework – March 2018

www.ifrs.org

Article 3:

What is the Coronavirus disease 2019 (COVID-19) & how has it impacted the world economy thus far? (31 December 2019 – 06 March 2020)

This article will be divided into two sections. Section 1 focuses on explaining, in a nutshell what the coronavirus and COVID-19 is, thereafter section 2 will explore its impact on the global economy thus far.

Section 1: What is the Coronavirus disease 2019 (COVID-19)?

COVID-19 or Coronavirus disease - 2019 is something that you would have seen and heard about on an hourly basis. It’s on every news network, social media network and on the lips of every individual worldwide. A phrase that has been uttered countless of time globally, and affects almost everyone on a global scale but are the details of this disease easy to understand and digest? Do we understand what it is and how to prevent it and are we aware of the impact it has had on the global economy?

A good starting point would be to have an overview of the coronaviruses themselves, what is it, how did it start and which of them are we currently dealing with?

The World Health Organisation (WHO) categorises coronaviruses (CoV) to be a large family of viruses that cause illness ranging from the common cold to more severe diseases such as Middle East Respiratory Syndrome (MERS-CoV) and Severe Acute Respiratory Syndrome (SARS-CoV). (World Health Organization: WHO, 2020)

Coronaviruses are zoonotic, and this means that they are transmitted from animals to humans.

Globally, we are facing an outbreak of a novel coronavirus (nCoV) which is a new strain that has not been previously identified in humans, this strain has taken on the acronym COVID-19 (Coronavirus disease – 2019) which was first reported from Wuhan, China, on 31 December 2019.

What is COVID-19?

COVID-19 is an infectious disease caused by severe acute respiratory syndrome coronavirus 2 (SARS coronavirus 2, or SARS-CoV-2), a virus closely related to the SARS virus. (Wikipedia, 2020)

COVID-19 is being spread person to person via respiratory droplets produced from the airways (nose or mouth) of humans during coughing, sneezing or exhaling. These droplets then accumulate on surfaces and objects around the person which are then transmitted to others via contact with these objects or surfaces, then touching their eyes, nose or mouth. COVID-19 can also be transmitted if they breathe in droplets from a person with COVID-19 who coughs out or exhales droplets.

The World Health Organisation (WHO) recommends staying more than 1 meter (3 feet) away from a person who is sick.

In order to protect yourself and your loved ones from the disease education on the disease is imperative. The World Health Organisation (WHO) has a list of protection measures for everyone which can be accessed here.

Section 2: How has it (COVID-19) impacted the world economy thus far?

Coronavirus disease 2019 or COVID-19 since it’s discovery in Wuhan, China on the 31st of December 2019 has had a negative impact on the global economy beginning with the disruption of China and moving progressively across the globe. The death-toll, the spread of the disease and impact on global markets thus far have been negative.

The World Health Organisation (WHO) has called the outbreak of COVID-19 a “public health emergency of international concern”

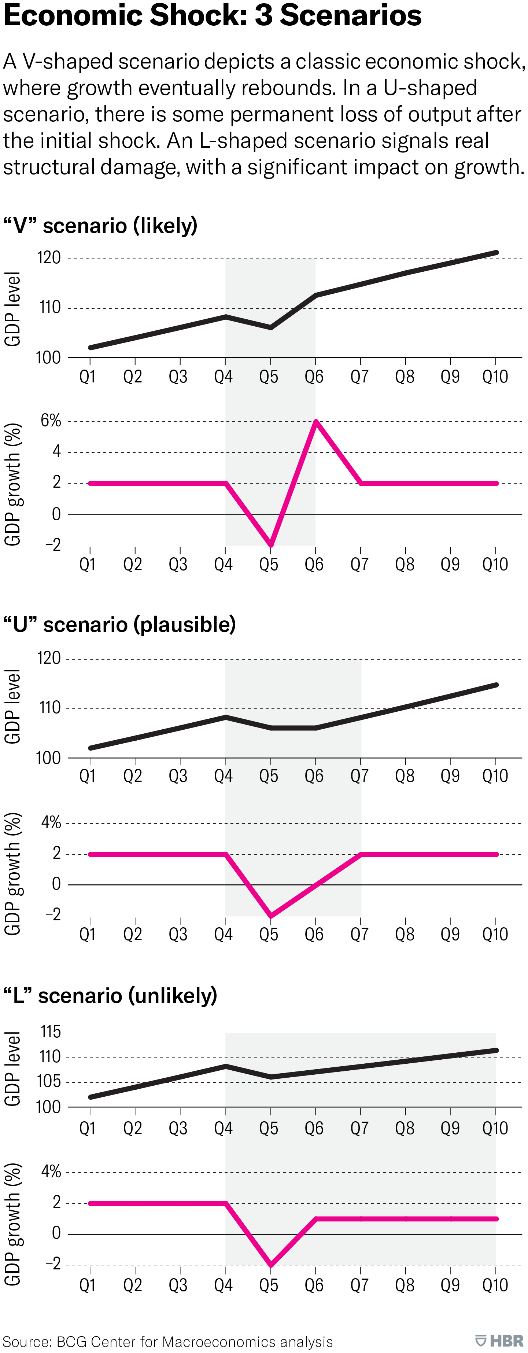

Bain & Company, as of March 5, have classified the disease a level 5 on the Bain’s Situational Threat Report (SITREP) Index which states that First-level contingency procedures should be activated (Bain, 2020). Bain & Company go on further to say that the Chinese supply chain has been severely affected by COVID-19 and economic indicators imply little improvement in output and that a rapid “V-shaped” recovery is becoming less likely by the day.

The highly uncertain nature of the disease and its evolution make it very difficult for policy makers to formulate appropriate macroeconomic policy response.

Dr Daniel Bachman of Deloitte Insights has stated that COVID-19 could affect the economy through three channels: a direct impact on production, supply chain and market disruption and a financial impact on firms and financial markets.

He has also formulated descriptive ideas about the possible paths the disease outbreak and global economy may take. These scenarios are: the worst is over, year of the virus, global pandemic response and financial crisis

To read Dr Daniel Bachman’s entire article on the economic impact of COVID-19 (novel coronavirus) click here.

According to CCN Business, as at March 6th 2020, the Coronavirus disease 2019 has wiped $9 trillion off stocks. CNN Business also reported that “S&P Global Ratings downgraded its economic outlook for Asia Pacific, saying the coronavirus could wipe $211 billion from household, corporate and government incomes and slow economic growth in the region to 4% for the year. The ratings agency had earlier forecast growth of 4.8%. (Business, n.d.)

"Our U-shaped recovery has been pushed back to later in 2020 due to a harder hit to China's economy in the first quarter, viral transmission outside China, and tighter financial conditions," the S&P economists wrote.

Overall, the state of the global economy is in decline and this is due to the fears of the coronavirus which have resulted in investor nervousness, so is there any good news?

Positives can be difficult to find in a situation in which people’s lives are being lost, however, in business terms there is some positivity. Consumer goods giant Reckitt Benckiser has seen a boost in sales for its Dettol and Lysol products (Brown and Palumbo, 2020). The price of gold - which is often considered a "safe haven" in times of uncertainty - has also increased. Its spot price hit a seven-year high of $1,682.35 per ounce in February (Brown and Palumbo, 2020).

These are small positives in a sea of negatives, however, the human spirit must persevere and continue to look for positives, adapt and overcome the current conundrum we find ourselves in.

List of References:

World Health Organization: WHO (2020). Coronavirus. [online] Who.int. Available at: https://www.who.int/health-topics/coronavirus.

Who.int. (2020). Q&A on coronaviruses. [online] Available at: https://www.who.int/news-room/q-a-detail/q-a-coronaviruses.

Wikipedia. (2020). Coronavirus disease 2019. [online] Available at: https://en.wikipedia.org/wiki/Coronavirus_disease_2019.

Bain. (2020). Tracking the Global Impact of the Coronavirus Outbreak. [online] Available at: https://www.bain.com/insights/tracking-the-global-impact-of-the-coronavirus-outbreak-snap-chart/ [Accessed 10 Mar. 2020].

Carlsson-Szlezak, P., Reeves, M. and Swartz, P. (2020). What Coronavirus Could Mean for the Global Economy. [online] Harvard Business Review. Available at: https://hbr.org/2020/03/what-coronavirus-could-mean-for-the-global-economy.

www2.deloitte.com. (n.d.). The economic impact of COVID-19 | Deloitte Insights. [online] Available at: https://www2.deloitte.com/us/en/insights/economy/covid-19/economic-impact-covid-19.html [Accessed 10 Mar. 2020].

Business, J.D., Sherisse Pham and Hanna Ziady, CNN (n.d.). The coronavirus crash has wiped $9 trillion off stocks already. Global markets are still falling. [online] CNN. Available at: https://edition.cnn.com/2020/03/05/investing/asian-market-latest/index.html [Accessed 10 Mar. 2020].

Brown, L.J., David and Palumbo, D. (2020). Eight charts on how coronavirus has hit the global economy. BBC News. [online] 6 Mar. Available at: https://www.bbc.com/news/business-51706225.

End.